Thank you for visiting this blog. Register or Login now to contribute.

Articles, letters and other publications by Christopher Ram

Dear Editor,

Yesterday’s (11 January 2026) Stabroek News carried a notice by Banks DIH Holdings Inc. convening its second Annual General Meeting for Saturday, 31 January 2026. The newspaper also reported that the company proposes to cap shareholder voting power at 15%.

No shareholder I have spoken to – including several members of staff at Ram & McRae – has received either the notice of meeting or the company’s annual report. An electronic copy of the annual report was, however, made available to me, having been downloaded from the company’s subsidiary’s website.

That circumstance immediately raises questions concerning the adequacy of notice and the distribution of the annual report. The Companies Act sets out a clear statutory framework governing these matters, and compliance with both the Act and the company’s constituent documents is not optional.

While that matter is important, I treat it as secondary. The more serious concern lies in one of the proposed resolutions and, in particular, the proposed amendment to the company’s by-laws.

The Notice states that “Article 8 of the By-Laws” is to be amended to impose a 15% cap on shareholding and voting power, with votes above that threshold to be rendered invalid and not counted. The proposal further provides for the aggregation of interests held by spouses, children, trusts, controlled companies and persons said to be “acting in concert”, establishes a special register, appoints a “Special Registrar”, and ultimately empowers the directors to compel the disposal of shares deemed to be held in excess of the limit.

This proposal is misconceived, constitutionally unsound, legally impermissible, and violative of the most basic principles of company law and the fundamental nature of a public company. It seeks, through by-laws, to do what the law permits, in appropriate circumstances, only by amendment of the articles of incorporation by way of a special resolution.

To begin with, there is a fundamental conceptual error. There is no such thing in our Companies Act, or in company law generally, as an “Article of the By-Laws”. Articles are mandatory constitutional instruments; by-laws are separate and secondary, generally confined to internal administration. They cannot define, restrict, or extinguish proprietary rights. The reference to “Article 8 of the By-Laws” therefore reflects not loose drafting, but disappointingly, a fundamental misunderstanding of the most basic principles of company law and the hierarchy of corporate instruments established by the Act: first the Act, then the Articles, and only then the by-laws.

More fundamentally, a restriction on voting rights or on the effective enjoyment of shares is a restriction on property. Under the Companies Act, such restrictions must be expressly stated in the articles and should appear on the share certificate. They cannot be imposed, enlarged, or enforced through by-laws, however carefully they are worded. A by-law cannot lawfully invalidate rights attached to issued shares, nor can it set conditions to their disposal. Even unanimous shareholder approval cannot cure an illegality.

But beyond illegality, the proposal is objectionable in conception. It is not even-handed. While it aggregates certain relationships to enforce the 15% cap, it ignores economically aligned companies that together exercise significant influence. That selectivity exposes the proposal for what it is: a mechanism to entrench existing control by neutralising potential rival shareholders.

Restrictions of this nature belong to the private-company model and, in those limited circumstances, require amendment of the articles by special resolution. In a public company, their effect would be to destroy its public character by undermining the free and proportionate exercise of shareholder rights.

There are additional concerns with the structure of the proposed resolutions. The prudent course is either to withdraw the Notice and reconsider the proposal, in which case a new meeting would have to be convened, or, if it is satisfied that the statutory notice period has been properly complied with, to withdraw the impugned amendment and proceed with the remaining business on the agenda.

That would ensure and demonstrate compliance and respect for the law, for shareholders, and for the integrity of the company’s governance.

Yours faithfully,

Christopher Ram

Business and Economic Commentary by Christopher Ram

Introduction

The Government of Guyana has announced that it has agreed to accept foreign deportees from the United States – persons who are not Guyanese nationals. The announcement was made calmly, almost casually – by one of the “family” – as if it were a routine domestic arrangement. There was no explanation of the legal basis for such an agreement, no disclosure of its terms, and no acknowledgement of its implications for Guyana’s immigration laws, internal security, or sovereignty. There was no parliamentary debate and no public consultation.

Yet this decision must not be treated as a technical matter. US President Doland Trump has made it clear that he does not regard international law, multilateral agreements, or established norms as binding on the United States, rejecting even frameworks that his own country previously championed. In Trump’s world, power is not limited by law or institutions but only by his personal morality — a position he has stated explicitly and acted upon repeatedly.

Trump world

It is against this backdrop of unilateralism, coercion, and transactional dominance that Guyana’s decision must be understood, not as a neutral administrative arrangement, but as an accommodation made in Trump’s world where rules are increasingly replaced by raw power. A world in which there is open contempt for international law (if at all), of multilateral institutions, and of the sovereignty of weaker states.

Donald Trump has already signalled his willingness to discard global norms at will. He has informed the OECD that the United States will not be bound by the 15% global minimum tax. He has pulled out of almost every international institution not in the US’ interest. And has made it clear that international rules apply to others, not to America. Power, in his worldview, is constrained only by his own judgement.

Nowhere is this clearer than in Venezuela.

Without even a murmur from our otherwise talkative CARICOM leaders, including our own President Irfaan Ali, Trump’s administration has used brute military force in the Caribbean, resulting in the deaths of civilians off the Venezuelan coast. U.S. forces seized the leader of a sovereign state and removed him and his wife in handcuffs. This was not multilateral action, not international law enforcement, and not humanitarian intervention. It was unilateral power, exercised openly and without restraint. The Caribbean as a zone of peace has become a zone of fear.

It is oil, stupid

From Trump himself, it is all about oil. The United States has effectively taken control of the world’s largest proven oil reserves. Trump has announced that Venezuelan oil fields will be restored, production ramped up, exports controlled, and prices influenced — with him deciding how much revenue will be returned to the Venezuelan people. This is not regime change in disguise. It is resource capture unlike any seen for more than several decades. It makes Afghanistan, Iraq and Grenada look like exercises in restraint by comparison.

Trump is not finished. He has shown himself willing to overturn democratic outcomes at home, to threaten friendly states abroad, and to redraw spheres of influence as if international law were an inconvenience. He speaks casually of peace with Russia while demanding a substantial share of Ukraine’s future in return. He does not need international law. He is international law. His narcissism has led to the so-called Donroe Doctrine, infinitely worse than the Monroe Doctrine of 1823 which the US claimed the Caribbean as its sphere of influence. But the Caribbean is not enough. He wants Greenland and maybe, later, Canada.

And it is at precisely this moment that Guyana appears eager not only to accept foreign deportees at Washington’s request, but also to deepen defence cooperation with the same administration now destabilising the region. We refused renegotiation of the 2016 Agreement in place of sovereignty. Now we surrender our dignity, our laws, our patrimony posing as neutrality.

More oil less money

That brings us to the most immediate and dangerous consequence for Guyana.

Donald Trump has announced his intention to use Venezuelan oil to drive the global price of crude down to US$50 per barrel. If he succeeds – and there is no effective international mechanism to prevent it – the impact on Guyana will be severe. At this price, Guyana’s oil revenue will collapse. The State would receive approximately US$1 per barrel in royalty and about US$7.50 in profit oil. With NRF funding accounting for 50% of the National Budget, we will experience increased and unsustainable budget deficits -or raid the NRF.

The Government would face three options, none of them attractive: heavy and expensive borrowing, sharp expenditure cuts, and drastic shortage of foreign exchange. Borrowing on that scale would undermine debt sustainability. Spending cuts would fall on wages, social programmes, infrastructure, and transfers – areas that have expanded rapidly in anticipation of sustained oil revenues.

Foreign exchange shortages would follow quickly. With oil inflows reduced, the supply of U.S. dollars would tighten just as import demand remains high. Pressure on the exchange rate would intensify. The cost of food, fuel, medicine, and construction materials would rise sharply. Inflation would not be a statistical abstraction; compounding the already his cost of living, the poor would suffer.

America hasn’t always been a friend of Guyana. Just read The West on Trial. As we turn our backs on countries that supported us during our darkest days, let us not forget our past. Guyana needs to face the dangers of the path of accommodation.

It must read the winds that can blow our house down. The finance minister hinted at an oil price adjustment in his mid-year report. That was before Trump had got his hands on Venezuela’s oil. The whole vision of One Guyana will evaporate.

Introduction

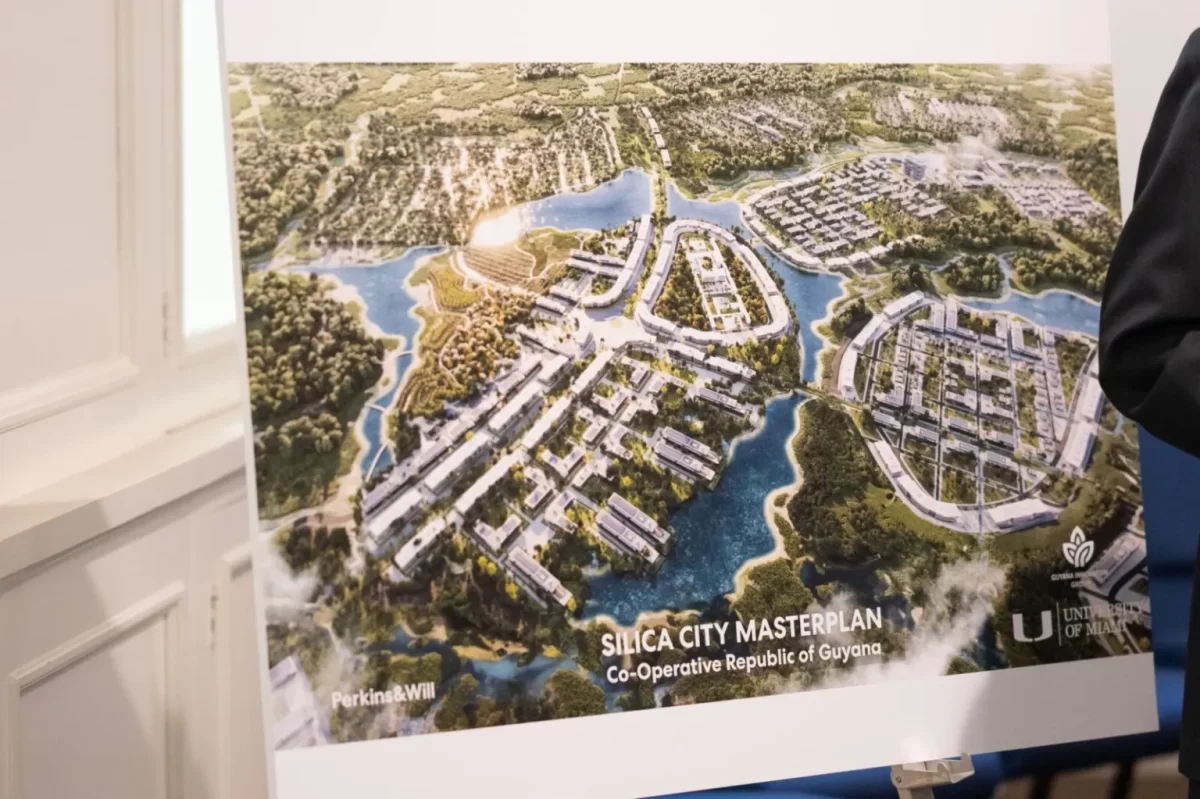

Other than periodic, campaign-style announcements, the Silica City project on the Soesdyke-Linden Highway operates in near-complete secrecy. It is repeatedly celebrated as the President’s “brainchild”, yet the public has been told nothing of how it is financed, how it is structured within government, or by what criteria the beneficiaries of its house lots will be selected. That pattern was maintained most recently as last week, when Collin Croal, Minister of Housing, announced that agreements have been signed and allocations of houses made, without accompanying disclosure of any legal authority, eligibility rules, pricing framework, or institutional approvals governing those allocations.

This silence is not accidental. Silica City has been variously described as a housing scheme, a “young professionals” enclave, a smart city, a decongestion strategy, and a commercial and healthcare hub. The descriptions shift with the audience – and with each statement. That is contrived confusion to avoid the project being pinned down to a single statutory regime, a single governance framework, or a single line of accountability. When a project is so flaky, when it begins to appear like a recycled scheme, it is time to raise the alarm.

We have seen this movie before. The Sparendaam housing project – Pradoville 2 – did not unravel by accident. The investigation showed that it was financed through multiple state entities, with no single institution carrying the full cost and no consolidated accounting of the project. That fragmentation diluted responsibility, obscured the true cost, and prevented scrutiny until long after land was transferred and beneficiaries entrenched. By the time the full picture emerged, accountability was already lost – and no one was ever held responsible.

The forensic investigation later showed how the absence of clear statutory footing, the bypassing of institutional processes, undisclosed allocation criteria, missing records, and political direction substituting for law produced outcomes that benefited a select few, including the then President, Ministers, party figures, and carefully chosen beneficiaries.

The project

Little has been said about Silica City’s administration, except that it appears to fall under the Central Housing and Planning Authority, established under the Housing Act, more noted for its outdatedness (1946) than for its relevance. The CHPA is a statutory authority governed by the Housing Act, with defined objectives – Housing of persons of the Working Class – procedures, reporting obligations, and safeguards designed to prevent the kind of opacity and looseness exposed by the Sparendaam investigation.

Yet, an enduring and necessary safeguard provided for under the Act has been dispensed with – too inconvenient for Silica City. Annual Reports have disappeared. There is no identifiable public accounting for the project. The project does not appear in the National Estimates, nor is it identifiable in the financial statements of the CHPA or any other government authority. This is despite the vast sums being spent on infrastructure and construction.

The chain of command compounds the danger. The Minister administering CHPA reports directly to Mohamed Irfaan Ali. There has been some reshuffling of junior ministers, but a party loyalist remains in charge. From all accounts, the administrative structure and key personnel unchanged. The result: a flagship housing project executed by CHPA under direct political oversight, with diminished reporting and no transparent disclosure of financing, governance, or allocation criteria. All in an environment of an explosion of funds accompanied by an erosion of accountability.

Loosening the reins of accountability

Since the PPP/C returned to office in 2020, CHPA has abandoned the comprehensive Annual Reports required by section 49 of the Housing Act, substituting bare audited financial statements that say nothing about projects, allocations, beneficiaries, or policy decisions. The stage was set: no meaningful statutory reporting. As a result, Silica City is rendered financially invisible to citizens and Parliament alike. This violation of the law shields the project from scrutiny while land is allocated, infrastructure constructed, and commitments locked in.

That this has gone undetected and unchallenged is itself a serious institutional failure. The Audit Office of Guyana exists to ensure compliance not only with accounting standards, but with the laws governing public authorities. The absence of Annual Reports, and the complete invisibility of Silica City in CHPA’s published accounts, should have been explicitly flagged.

Equally troubling is the silence of the National Assembly of Guyana, at least some of whose members know that the Housing Act requires far more than numbers stripped of context. When a statutory reporting framework collapses in plain sight, unnoticed by auditors and unchallenged by Parliament, accountability disappears, and lawful administration collapses.

President Ali

At this point, it is no longer credible to discuss Silica City without addressing the common role of President Ali himself. The Sparendaam investigation did not describe a single rogue decision or a momentary lapse. It documented an infrastructure of persons and practices through which housing projects were executed: political direction overriding statute, institutions reduced to conduits, records absent or reconstructed after the fact, and accountability dissolved by design.

What makes the current project more troubling is that many of the same enabling conditions have re-emerged on a far larger and more expensive scale. Then, Dr Ali operated as Housing Minister under a President. Now, he is the President. Then he reported to Cabinet. Now, Cabinet reports to him.

Silica City is framed as a legacy project. But vanity cannot come before legality, and legacy cannot be built on secrecy, evasion, and disregard for statutory accountability. History is unforgiving on this point. It judges leaders not by the size of their projects, but by whether those projects followed the law, the institutions of the state, and earned the public trust.

Conclusion

Having been involved in the investigation into the Sparendaam project, I recognise the warning signs. I fear that if this project is allowed to continue under existing conditions of opacity, avoidance of scrutiny, and deliberate invisibility, we will not later be wondering whether Silica City was Pradoville 3.

We will already know the answer.

Dear Editor,

In announcing his appointment of members to the Teaching Service Commission (TSC) without consulting the Leader of the Opposition, President Ali explained that no consultation was possible because no such Leader had been elected since the elections, and that conditions in the education sector required immediate action. In substance, the President was asking the public to accept that constitutional compliance could be set aside in the name of urgency and the public good. That is a bitter pill to swallow.

The Constitution does not suggest or invite consultation with the Leader of the Opposition: it commands it. The constitutional office of LOO is not ceremonial, ornamental nor optional. It is intended to place a restraint on executive power in a winner-take-all constitutional system and to ensure that constitutional commissions operate independently and professionally, representative of the society rather than as proxies for the government of the day. By ignoring this constitutional mandate, the appointments to the TSC are not merely irregular; they are constitutionally tainted – and dangerous.

On inspection, the President’s announcement rings hollow. As a senior member of the Bar observed in another context – that of the mysterious exit of the former acting Chancellor – procedural silence often conceals mischief. The prolonged failure to have a Leader of the Opposition elected raises identical concerns. This is not conjecture; it is a conclusion supported by deliberate inaction and disturbing, verifiable facts.

The elections are over. The recess has been taken. Parliament is sitting. A speaker has been elected. Opposi-tion members are present and calling for the election. The Speaker first disappears and then, acting with the political comfort of his sponsors strengthened by an enlarged government majority, blatantly refuses to facilitate the election. This is not inadvertence. It is obstruction. The vacancy advanced by President Ali to justify his constitutional violation, has been engineered, maintained, and is now being cynically invoked by the President.

What is being presented as constitutional impossibility is, in truth, constitutional engineering.

The President has attempted to cloak this manoeuvre in urgency, pointing to staffing pressures within the education system. He spoke of some 2,700 senior vacancies to be filled, including more than 800 newly created senior posts that did not previously exist. The suggestion was that events had overtaken constitutional formality. But the 2025 Estimates expose that claim. Education staffing spans Agency 40 and all ten regions. Its levels, scales and senior layers were known, budgeted for and deliberately restructured. These pressures were not sudden. They were foreseeable and, in significant part, policy-driven.

That makes the invocation of urgency disingenuous. Senior vacancies do not arise overnight; they build up over time and should have been addressed long before they became a constitutional excuse. The urgency claim also clashes with the Government’s own rhetoric. In his 2025 Budget Speech, the Minister responsible for Finance boasted of a transformative education agenda, and in the debate the Minister of Education praised the PPP/C’s record in the sector. Neither spoke of crisis. A government cannot celebrate success in one breath and plead constitutional necessity the next.

That contradiction matters, because this is not the first time “necessity” has been pressed into service to excuse constitutional shortcuts. In 2022, the appointment of Clifton Hicken as acting Commissioner of Police was defended on the basis that consultation with a Leader of the Opposition was impossible because none existed—an explanation accepted as exceptional at the time. Following the 2025 elections, the same rationale has been recycled, with Parliament once again allowed to remain incomplete so that constitutional consultation can be declared impossible.

The pattern extends beyond appointments. Nowhere is constitutional disregard more visible than in the administration of the Access to Information Act, enacted to give effect to the constitutional right to information. For years, the Commissioner of Information has failed to provide responses to requests or meaningful oversight, while reporting and enforcement have all but disappeared. This inaction has been tolerated rather than corrected—an omission made more troubling by the fact that the President himself holds the portfolio of Minister of Information. What is presented as bureaucratic failure is, in truth, constitutional neglect at the highest level.

Viewed together, these episodes point to a clear strategy by President Ali: constitutional constraints are not confronted but systematically weakened. When compliance is inconvenient (access to information), institutions are allowed to fail; when consultation is required (the election of the Leader of the Opposition), the conditions for it are deliberately left unmet; and when challenged, necessity is invoked after the fact (the Teaching Service Commission).

This is not governance; it is the erosion of the Constitution and the gutting of the rule of law.

The Teaching Service Commission appointments therefore raise more than a legal issue. They raise a democratic one. The failure to empower the opposition does more than narrow political inclusiveness; it contributes to what Nobel Prize–winning scholars describe in Why Nations Fail as the drift toward an extractive political system.

Yours faithfully,

Christopher Ram

Business and Economic Commentary by Christopher Ram

Introduction

On November 26, 2025, Stabroek News reported Senior Minister with responsibility for Finance, Dr Ashni Singh, as saying that he was “still awaiting a clear update” on the long-delayed 2022 Population and Housing Census, that he was unsure what caused the delay, and that he intended to raise the matter with the Chief Statistician “very soon.” Such an explanation might pass from an ordinary minister. Dr Singh is not. It might also be excusable if the issue were routine. This particular census is neither. And it might still be tolerable if the delay were brief. It is now measured in years.

For all these reasons, Dr Singh’s explanation is bewildering at best. He has the honour – and the responsibility – of presenting annual budgets exceeding one trillion dollars, allocating resources across an expanding landscape of ministries, departments, agencies, regions, and sectors.

That task demands the most current and reliable demographic and socio-economic data available. It cannot responsibly and properly be discharged by guesswork, political preference, or incremental increases carried over from the past. A population and housing census is precisely the dataset that anchors such decisions. For the Senior Minister responsible for Finance to accept – assuming his account is accurate – a state of affairs in which that foundational data is unavailable, unexplained, and unmanaged is not merely regrettable. It borders on incredible.

The explanation is not merely puzzling in a political sense; it is difficult to reconcile with the statutory framework governing official statistics in Guyana. The Statistics Act does not contemplate an open-ended census process, nor does it permit foundational national data to drift indefinitely without explanation or accountability. Censuses are not peripheral outputs. They are universally regarded as core state functions.

The statutory, governance framework

The Bureau of Statistics does not operate in isolation. It is governed by a Board chaired by the Finance Secretary – who operationally reports direct to the Minister – with the Chief Statistician as Vice-Chair, and comprising senior public officials. Oversight of the Bureau therefore sits squarely within the financial and administrative architecture of the State. Delays of this magnitude cannot occur unseen, unexplained, or unmanaged at that level.

Nor does responsibility end with Dr. Singh. In a move that is unprecedented, was never explained, and is not clearly understood, President Ali has not allocated finance to its own minister. Under our constitutional framework, Finance is therefore retained within the Office of the President, and responsibility for Statistics has been allocated to no other minister. In such circumstances, prolonged non-delivery cannot be treated as an operational mishap. It becomes an executive failure that points directly to Dr. Singh and indirectly to President Ali.

What makes this failure especially troubling is that in response to calls for the report to be published, the public have been fed with a mixture of excuses and promises have been made for the release of the report. This is no longer a single lapse. It is a pattern. Years have passed and another beckons. The Census has now outlived one Board of the Bureau of Statistics and is approaching the end of the tenure of its successor. The impending expiry of the current Board heightens that failure. A governing body chaired by the Finance Secretary, with the Chief Statistician as Vice-Chair, and populated by senior public officials, will have completed its term without delivering the most important statistical output of the decade.

Boards are appointed to govern, to supervise, and to ensure delivery. When a board’s term expires without results, responsibility gives way to accountability – not excuses. It does not roll forward automatically to the next appointment. This is therefore a moment of reckoning. As 2025 draws to a close, the continued absence of the 2022 census cannot be treated as an inherited problem, a technical delay, or a matter awaiting engagement “very soon.” Without the proverbial bogeyman of the PNC or the Coalition, the ownership of this failure – spanning years, boards, and budgets – belongs 100% to the Ali Administration. At year-end, responsibility cannot be deferred any further – it must be owned and acted upon.

Broader functions in peril

What makes this failure even more troubling is that the Statistics Act does not contemplate a single, isolated census. It provides for several distinct censuses and large-scale statistical exercises – including population and housing, labour force, household expenditure and other socio-economic surveys – each separate in scope, but all essential to decision-making, public administration, and management applying evidence-based governance. The Act also gives the Bureau latitude, with ministerial approval, to undertake additional censuses and surveys as circumstances require. In other words, the population and housing census is not the sole output of the statistical system, but the cornerstone upon which the others rest.

The prolonged non-delivery of that cornerstone therefore raises unavoidable questions about the wider statistical architecture of the State. If the most comprehensive, best-resourced, and most anticipated census cannot be brought to completion and publication, what confidence can be placed in the timeliness, reliability, or even the existence of other censuses mandated or permitted by law? Planning on social and physical infrastructure, skills requirements and availability, poverty measurement, household consumption analysis and intercensal estimates all depend, directly or indirectly, on the population baseline. The failure to publish the 2022 casts a shadow over the entire system of official statistics and weakens the informational foundation on which policy decisions are made and national finances are allocated.

There is an additional and more troubling consequence of this prolonged inaction. In the political sphere, the absence of inconvenient data may be tolerable, even advantageous. It allows narrative to substitute for evidence, delays scrutiny, and permits claims of progress to go largely untested. In management, however, the same absence is dangerous. Decisions made without reliable baseline data distort priorities, misallocate resources, and entrench inefficiencies. Political convenience in the short term is almost always harmful in the long run.

Conclusion

As the year draws to a close, this matter can no longer be left to drift. The imminent expiry of the current Board makes inaction dangerously unacceptable. If the 2022 Population and Housing Census is to retain any value, the President and the Senior Minister responsible for Finance must act decisively: appoint a new Board without delay, with a clear and public mandate to bring the exercise to publication within a fixed timeframe.

Anything less would constitute a governance failure that has already persisted far too long.