Introduction

If we look across the Caribbean we see a number of companies that have extended well beyond their borders with Grace Kennedy, Republic Bank and Trinidad Cement being very prominent, burnishing their Caribbean credentials by cross-listing on the regional stock exchanges. Perhaps reflecting their growing confidence and strength, Trinidad and Tobago companies appear the most enterprising as their domestic market becomes more saturated forcing them to seek new opportunities and markets abroad. With the USA’s plans to follow International Financial Reporting Standards in place of US GAAP it may not be long before we see a Caribbean company seeking listing on a US stock exchange.

Where does Guyana stand among Caribbean companies having established one of the early companies (Banks DIH) to have gone into wide public ownership and with veteran entrepreneur Yesu Persaud regarded as one of the leading private sector persons in the region?

It seems not very far, defying all the hopes that the launch of the Guyana Stock Exchange and a very favourable tax regime for public companies would see an increase in the number of companies listing on the stock exchange, raising money from the public and providing the platform for take-off.

Going private

Instead the relationship between the Guyana Securities Council and leading public companies is at best strained; no company has yet listed and the quality of corporate governance is still strained. In fact, with public companies such as Guyana Stores, JP Santos and Hotel Tower Limited coming under limited personal or family control, it would probably be truer to speak of ‘going private’ rather than ‘going public.’

It may have been pure coincidence that Banks DIH was again in the forefront among local companies to have offered a significant share to a foreign company – Banks Barbados – although the purpose may have had little to do with regional co-operation. It is difficult to say how beneficial the move was to the company as a whole, but it was both bold and novel to see truly outside directors with real clout being placed on the board of any public company in Guyana.

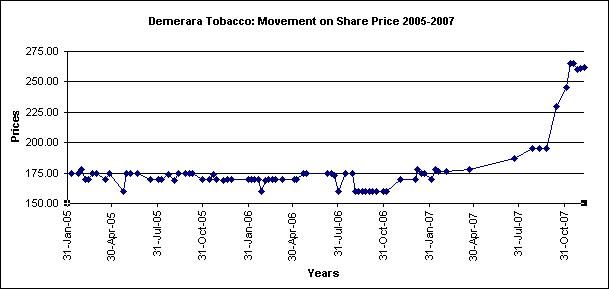

The other major public company with wide-shareholding – DDL – has not only not done well in its overseas ventures, but many of its new ventures have been as private companies not subject to the higher standards of transparency and disclosure applicable to public companies. Worse, the company like so many of its counterparts seems to take the approach of the goldfish, unable or unwilling to see any wart that would restrict its own development, no matter how obvious to even the most casual observer.

Of course the government has abandoned its commitment to widespread public ownership and Guyanese can only dream of a stake in any of those companies which are being given all sorts of goodies to ‘encourage’ them to risk exploiting our natural and sometimes non-renewable resources. While we ask the government to comply with the Investment Act in relation to local private sector companies, we should not lose sight of the danger of worse excesses taking place in relation to foreign companies. These deals which can bind the country for decades should be tabled in the National Assembly in the interest of transparency and to reassure those investors.

Competing at more than cricket

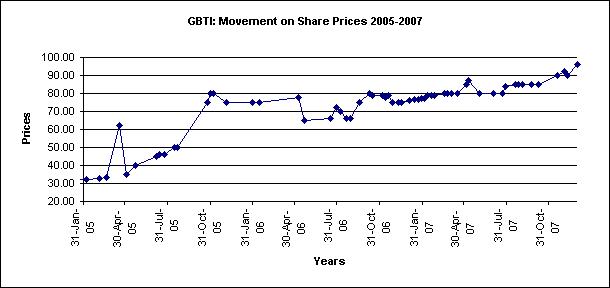

But back to our private sector companies and whether they have what it takes to compete regionally and internationally to take on and beat the Bajans, Trinis and Jamaicans, like we do in cricket – at least some of the time. GBTI is a sound financial institution that can move outside of the Guyana market, but nothing that the directors have said suggests that they are thinking in that direction.

What a boost it would be for Guyana to hear that our own GBTI has taken majority control of another regional financial institution. Or that Bakewell – a private company – has moved into another market. Indeed these are legitimate questions to any entrepreneur who laments the domestic business environment.

Seeking answers to these questions I turned to my favourite and best-selling business book, Built to Last: Successful Habits of Visionary Companies by Jim Collins and Jerry I. Porras, which was followed up by a solo effort by Jim Collins: Good to Great: Why Some Companies Make the Leap . . . and Others Don’t.

Included in Built To Last, are eighteen companies the authors identified as a “visionary company,” defined as one that is a premier institution in its industry, is widely admired by knowledgeable businesspeople, made an imprint on the world, had multiple generations of chief executive officers (CEOs), had multiple product/service life cycles, and was founded before 1950.

Good habits

In a summary of the book the Vance Caesar Group, ‘Premier Leadership Coaching,’ identified as the key question which Messrs. Collins and Porras sought to answer as “what has enabled some corporations to last so long, while other competitors in the same markets either struggle to get by, or fade away after a short period of time?” Collins and Porras took as their benchmark 18 well-known, well-established and healthy companies (‘visionaries’), and compared them to a counterpart in their specific area of business using as yardsticks common patterns and differences between their company and the counterpart. The result was a set of guidelines and principles that all companies, large or growing, can use to keep themselves growing, strong, and ahead of the competition.

Here are the outstanding features of companies that are built to last.

Clock builders, not timekeepers – They are focused on building the organisation so it would run “as smooth as a clock.” Visionary companies lead, not follow – build not watch the clock.

Have a set of core values – They began with a set of core values that persist and are practised at every level in the organisation, in good times and bad.

Have a core ideology – While the core value stays the same, the core ideology changes, preventing the company from being left behind and eventually disappearing. This is not the same as responding to every fad that comes around and usually takes place slowly, but fast enough to keep ahead of the competition.

BHAG (Big hairy audacious goals) – Not all shifts are incremental. Companies that are built to last periodically undergo paradigm shifts in products, and have clear-cut, compelling, cutting-edge goals the company sets to climb the next mountain.

Have a ‘cult-like’ culture – Everyone in the company must commit to the same core ideology, must be indoctrinated into the company culture, must develop a tight fit with others in the company, and must think of themselves as the ‘elite’ in their field.

Don’t be afraid to evolve – Visionary companies monitor trends, do their research and anticipate and even create changes. They do not wait on the market or on some other visionary before making their move.

Look inside for top management – Visionary companies have management development processes and succession plans in place to ensure smooth transitions and direction as the company ages. It is not unusual to find a defined succession plan that is more than one level deep, capable of responding to the most dramatic shock without any noticeable disruption.

Constantly innovate – Without this, the company’s products/services become obsolete and lead to a decline.

How have BTL companies fared?

Are the companies identified in the book still considered “Built to Last”? The answer depends as always on who is asked. Converts to the ‘Book,’ which they spell with a capital ‘B,’ would point out that every one of the 18 companies cited is still in business, is still a household name doing what they were doing decades before. Taken as a basket, these companies are also doing quite well in terms of total shareholder return, even though the writers themselves say that the companies were not selected on the basis of stock market performance.

Cynics not only point out that the shares of Motorola and Sony have lagged on the S&P 500 Index while Disney has taken a long time to recover from a long slump, but that the test was so widely framed as to allow too much latitude. At least 7 of BTL’s original 18 companies have stumbled, prompting the question, have companies struggled because they ignored the principles in the book or because they followed them?

Of more direct interest is the book’s relevance to our own entrepreneurs who are mostly self taught in the school of entrepreneurship, and whether the principles that may have contributed to the success of mainly US companies can be applied to Guyana where the business culture seems so different from the Caribbean, let alone the USA.

If Guyana is to compete then our companies – big and medium-sized – would need some paradigm shift in how they see their businesses. How our entrepreneurs respond will shape the Guyana economy for the next few decades.

Next week: Business Page’s response to the statement by the Ministry of Finance on the Queens Atlantic II Group and related matters.