Token GRA tax receipt helps Hess avoid paying taxes in the US

Introduction

In this Part 99, we address our attention to the 2021 audited financial statements of Hess Exploration and Production Guyana Limited (the branch) which despite its name, is in fact a branch of a Cayman Islands incorporated subsidiary of the American oil major Hess Corporation headed by John Hess. Of the heads of the three contractors under the 2016 Petroleum Agreement, Mr. Hess is by far the most open, even garrulous, when it comes to Guyana. But not without reason.

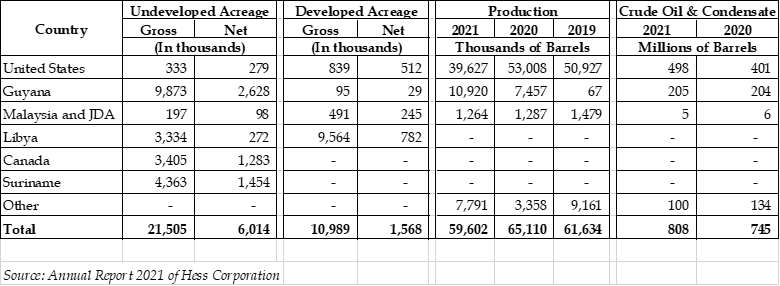

Guyana is the jewel in Hess’ crown, its cash cow, its redemption and its future. From ground zero two years ago, Guyana accounted for more than 25% of the Corporation’s global crude oil production in 2021, even as Hess has seen its North American production decline by more than 20% between 2019 and 2021. And of the Corporation’s gross and net undeveloped acreage, Guyana represents 45.9% and 43.7% respectively while 25% of the proved reserves of crude oil and condensate the Corporation is situate in Guyana.

Malaysia and JDA: Malaysia – Thailand Joint Development Authority.

That elusive tax

The taxation information is at once revealing and a vindication of the fears of commentators. The Statement of Consolidated Income shows a tax charge of US$600 million but that includes the amount of US$113 million “paid” by the Government of Guyana on behalf of the local branch for which Hess gets a token receipt. In a discussion on taxes, the Report informs the reader that the tax charge in 2021 was “primarily due to higher pre-tax income in Libya and Guyana”. The report also shows that income tax attributed to Guyana and Libya accounted for 92% of the taxes shown as a charge in Hess’ report for 2021. It is unclear whether the amount of US$436 million shown as paid in Libya in 2021 was a paper transaction as is the case with Guyana but given Libya’s sensible and logical position with oil companies, it is unlikely that that country’s political leaders would be as shamelessly obsequious to the oil companies as leaders Guyana and its leading politicians have always been.

It would be ironic but not surprising if, in the near future, the lion’s share of taxes payable in the Hess world comes from Guyana! Note 15 to the Report leaves no room for speculation or deduction – Hess paid no taxes in its home country from which it derives two-thirds of its crude oil production! Yet the oil companies are willing to argue in the Guyana courts that if they have to pay tax in Guyana, their business will suffer.

But things are so good for John Hess and the shareholders that in his letter to them he confidently predicted that all four of the Corporation’s production assets would be free cash flow generative in 2022 and is positioned to grow its cash flow at a “compound rate of 25% per year out to 2026”. It only gets better: with Liza Phase 2 beginning production in February 2022, at capacity, Hess is expected to add more than $1 billion of net operating cash flow annually, having repaid the remaining $500 million of its term loan; distributed a 50% increase in quarterly dividend; and committed to return up to 75% of its adjusted free cash flow annually to shareholders by increasing dividends and accelerating share repurchases.

And to think that Hess has less than one-third interest in the Stabroek Block. But Hess, and even more so Exxon, enjoy such confidence and respect of this country’s Government and the Opposition that they are proud to boast of their cooperative relationship with the oil companies and defend the iniquitous contract.

Let us now turn to the financial statements of the Guyana branch in which all figures in Guyana Dollars, unless otherwise stated.

Table of Income Statement

Crude contract, crude share

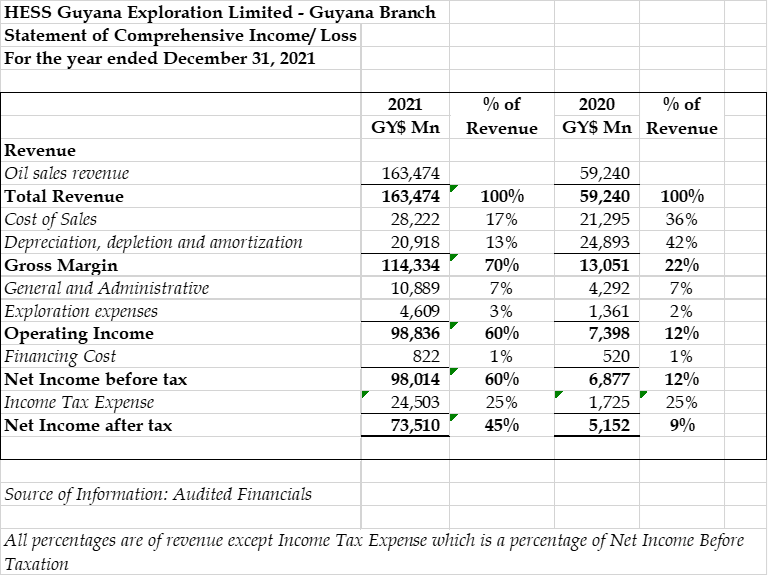

Using information in the Hess Corporation’s report on average price earned from Guyana crude, the branch sold approximately 11.4 million barrels in 2021, compared with about 6.1 million barrels in 2020. The financial statements of the branch state that it had no related party transactions in 2021, suggesting that those who direct the sale of the branch’s production bypassed the Group’s marketing subsidiary and chose other outlets to sell its share of profit oil and recoverable costs.

From the $163,474 million, deductions are made for Cost of Sales $28,222 million (17% of sales revenue) and Depreciation, depletion and amortisation (DPA) of $20,918 million (13% of sales revenue), leaving a gross margin of $114,334 million or a staggering 70%. A separate note shows that cost of sales is made up of production expenses of $25,635 million, royalty of $$3,923 million and change of inventory of $1,337 million. Royalty as a percentage of sales works out at 2.40%, compared with 2% provided under the Petroleum Agreement. The DPA is made up of $20,874 million in respect of development assets, representing approximately 5% of development assets, and $44 million on Leasehold assets, representing 4% of those assets.

Note 5 states that additions to Property, plant and equipment include the impact of new provisions and revisions for decommissioning obligations.

Deductions are also made for General and Administrative expenses of $10,859 million, up from $4,292 million in 2020, and include pre-development costs of future projects, and Exploration expenses of $4,609 million, up from $1,360 million, suggesting multiple cases of the productive operations carrying the cost of exploration activities. This violation of accounting, taxation and petroleum principles activities would not be tolerated anywhere except Guyana.

The insane Petroleum Agreement

The income statement also shows financing cost of $822 million, up from $520 million in 2020, a sum which also appears in the note on provisioning in the balance sheet. After all these costs are deducted from revenue, the Branch reports net income before taxation of $98,013 million (2020 – $6,877 million), which but for the Petroleum Agreement would be subject to Corporation tax (25%) and to withholding tax (20%) on the deemed distribution branch profit tax (BPT). A deemed distribution is the balance of profit after the Corporation tax less any re-investment of such profits, subject to the approval of the Commissioner General.

The Agreement also states that such tax must be included in the taxable income of the Contractor, meaning that the $98,013 million has to be treated as if it is a post-tax amount, requiring grossing up.

Since the Agreement exempts the oil companies from the BPT, the Branch then deducts the 25% from the profit, or $24,503 million, (2020 – $1,725 million) as though it is an actual sufferance rather than a benefit to be grossed up under Article 15.4 of the Petroleum Agreement. Hess the parent then gets a double benefit by claiming it as overseas tax paid in its US financial statements.

Using its own brand of phoney accounting which treats a benefit as a charge, Hess records a Net Income after tax of 45%, instead of 70%.

Balance Sheet

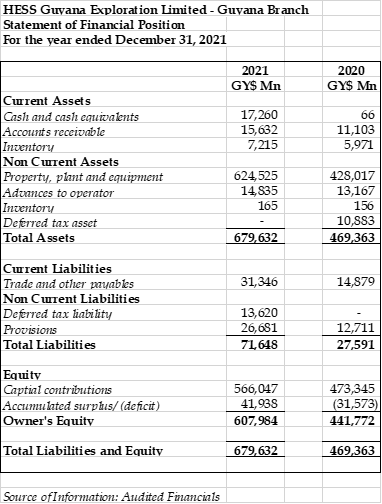

The total value of assets of the Branch at yearend was $$679,631 million ($469,363 million) of which Property, plant and equipment accounted for 92%, with the remainder spread fairly evenly over cash, receivables and advances to operator (Esso). At December 31, the amount of such advance was $14,834 million while Trade and other payables of $31,346 million, (2020 – $14,879 million) “mainly relate[d] to amounts owing to [Esso]”.

The Branch’s cash resources stood at $17,260 million, a substantial increase from the $66 million at December 31, 2020, while its commitments for capital expenditure on the Stabroek Block was “approximately $607,000 million (US$2,900 million), up from G$544,000 million (United States Dollars: $2.6 billion), “to be incurred over the next several years”.

Conclusion

As it was in 2020, the financial statements reveal very little by way of disclosure. Readers are no better informed of what makes up exploration, operating costs, and the less significant general and administrative. Even the most ordinary company in Guyana produces financial statements that are more informative, reader-friendly and superior to those of Hess’ Guyana branch. What is particularly noticeable, is that the financial statements of the Hess branch are neither consistent with those of its parent abroad or of any of its joint venture partners locally.

Next week’s column will feature the financial statements of Esso Exploration and Production Guyana Limited.